The Plan: It starts with the Strategic Plan or IDP which sets long-term goals. These goals become the APP or SDBIP for this year. The budget provides money to support these yearly goals.

The Link: Check if this year’s budget paid for the APP/SDBIP goals and see if actual revenue and spending matched delivery. Compare this information to the APR to see if the goals were achieved. If project spending is always lower than planned, it may mean delays or delivery problems. This can affect long-term goals.

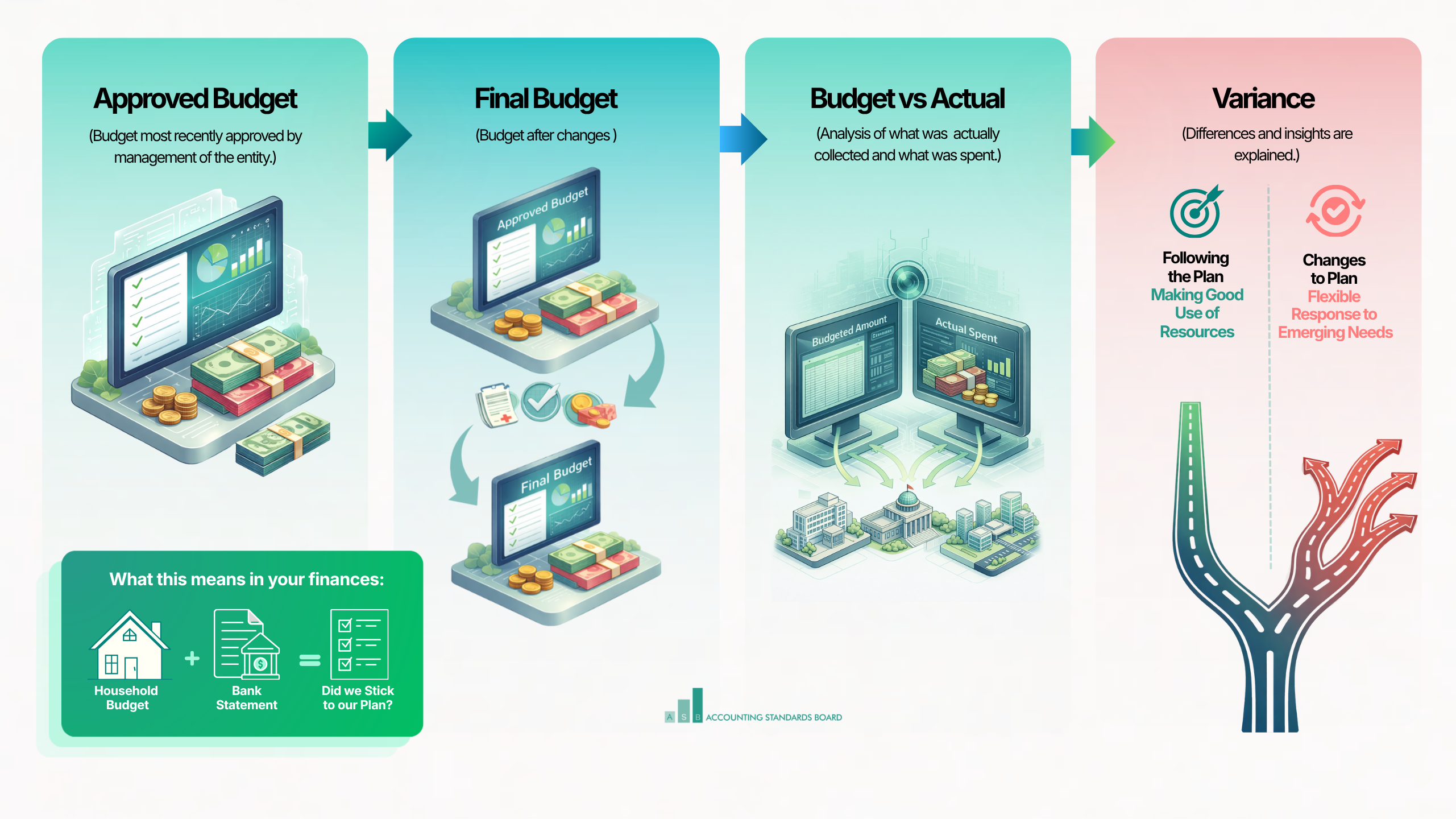

The Plan: The budget sets targets for all expected revenue sources like taxes, grants, and fees. It also sets targets for all the spending for the year.

The Link: The actual amounts come from the Statement of Financial Performance. They are adjusted to match how the budget was first made. This includes:

- The accounting method used (like cash instead of accrual);

- How items were grouped (by programme or department);

- The entities included in the budget; and

- The layout of the budget table.

It shows what the government owns and what it owes to others.

The Plan: There is usually no “Budgeted Balance Sheet,” but you can find the government’s plans in these documents:

- The Capital Programme – Shows the plans to buy, build, or fix assets (like land, buildings, roads or machinery).

- The Borrowing Plan – Shows how much new debt they plan to take on.

- The Cash Policy – Shows how much “emergency savings” they plan to keep in the bank.

The Link: Capital Programme: When you compare the plan to the actual amounts (on a comparable basis). You should compare the capital expenditure in the budget to the amounts in the Notes to the Financial Statements that show additions to PPE, Investment Property, Heritage Assets (adjusted to be comparable).

Look for these two main situations:

- If they spend less than planned (underspending) – This often means projects (like a new bridge or school) were delayed. It may look like the government “saved money,” but the community is actually losing out on a service that was promised.

- If they spend more than planned (overspending) – If the government overspends on its daily costs or loan payments, it has to get that money from somewhere. This usually means:

- Draining the bank – They use up their cash “savings.”

- Borrowing from tomorrow – They take out more loans, which means future budgets will have to pay for today’s overspending leaving less money for new services.

Borrowing Plan: Compare what is in the budget to the Non-current liabilities shown in the Statement of Financial Position. The Notes to the Financial Statements will show what debts were taken during the year.