How the Money Changed Over Time

(Statement of Changes in Net Assets)

Seeing how the total value of what the government owns changed after all income and expenses were settled.

What is it?

The Statement of Changes in Net Assets is a link between the Statement of Financial Performance and the Statement of Financial Position. It shows how the government’s financial position changed over the year.

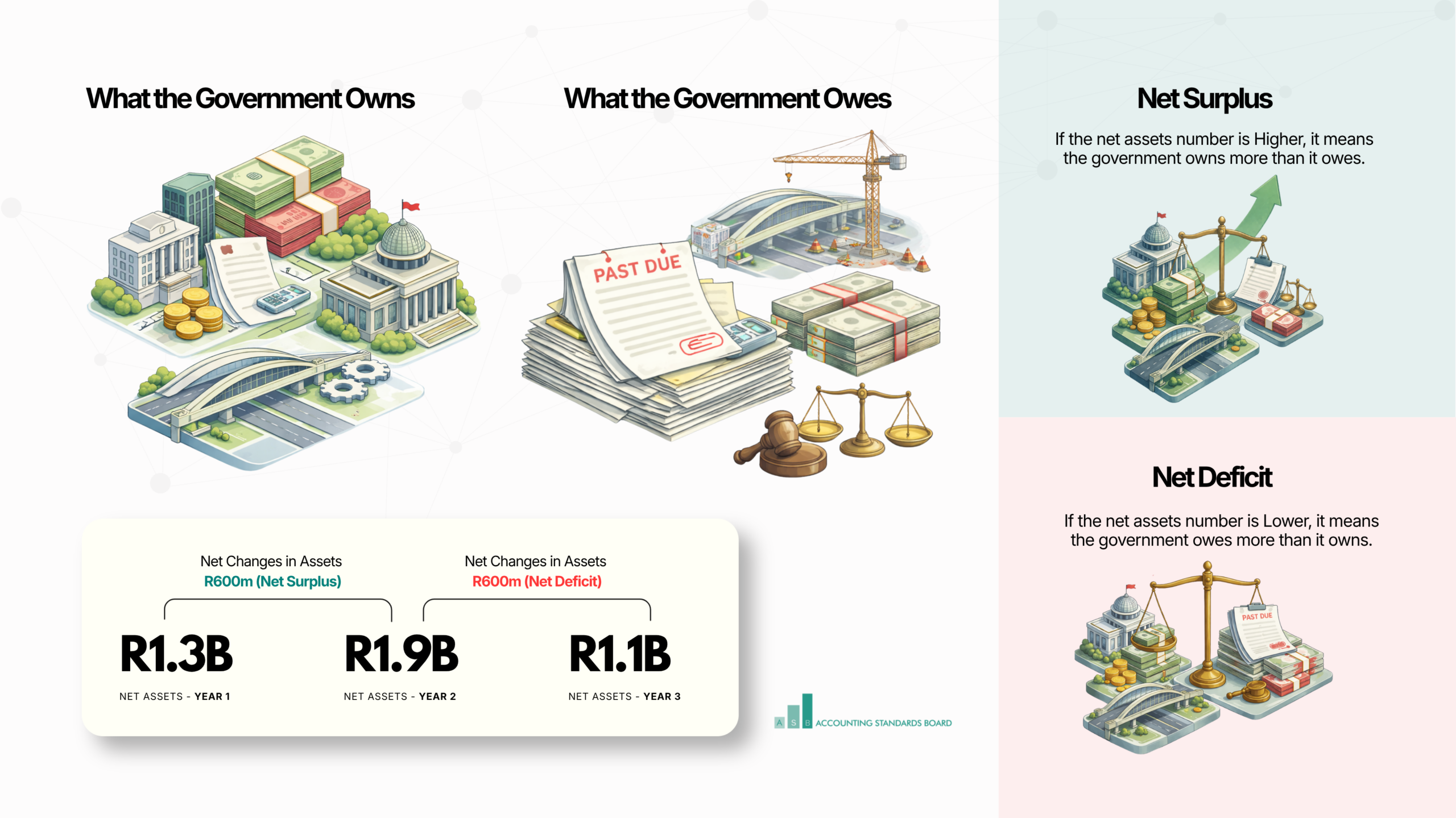

Net assets are the difference between what the government owns and what it owes. They include cash and other assets, not only the money in the bank. This statement shows how the government’s net assets changed during the year. This helps track the government’s net worth over time.

If the net assets number is higher, it means the government owns more than it owes.

How do net assets arise?

The Statement of Changes in Net Assets shows:

Opening Balances

What the government had at the start of the year.

–

Changes during the year

- Surpluses or Deficits

- Changes from Transactions with Owners

- Corrections of Past Mistakes

- Changes in Accounting Policies

- Revaluation Reserves

=

Closing Balances

What the government is left with at the end of the year.

These changes explain how the opening balance became the closing balance.

Net assets can change for several reasons:

The surplus or deficit for the year is the final result shown in the Statement of Financial Performance.

In the Statement of Changes in Net Assets, that result is added to the accumulated surplus or deficit. If there was a surplus, the accumulated balance grows. If there was a deficit, the accumulated balance becomes smaller.

Over time, this balance shows if the government’s financial position is getting stronger or weaker.

Sometimes the government may move some of their extra money from accumulated surplus into special savings called reserves. These could be housing reserves or capital replacement reserves. This is done to set the money aside for a specific purpose. These moves happen within net assets and do not change the surplus or deficit for the year.

Most government entities do not have owners like private companies. Some entities, however, have a “parent” in government. For example, a national department may act as the owner of a public entity.

Sometimes the parent-owner gives money to the entity. This may be to help it clear old loans or make its financial position stronger. This type of money is called an owner contribution.

The contribution increases the entity’s net assets, but it is not recorded as revenue. It also does not affect the surplus or deficit for the year. This is because the money was not earned from providing services. It was given by the parent-owner to support the entity.

Owner contributions are different from a grant or transfer. A grant is money given to pay for programmes or build assets like clinics, roads, or schools. Grants are recorded as revenue in the Statement of Financial Performance. They increase income for the year and affect the surplus or deficit.

This difference is important because:

- Owner contributions – Show support from the owner. They do not show how well the entity performed in delivering services.

- Grants and transfers – These are linked to operations or projects. They form part of the entity’s performance.

This difference helps citizens see if the government can support itself, or if it relies on extra help from its parent-owner.

Sometimes government finds a mistake in records from a previous year. The financial statements for that year would already have been finalised. Thus the mistake cannot be corrected through the current year’s surplus or deficit.

Instead, government adjusts the opening balance of net assets. This method is called a restatement.

A restatement fixes the past numbers as if the mistake never happened. This helps make sure that the current year’s results show only the current year’s activities and are not affected by past errors.

The details of these corrections are explained in the Notes to the Financial Statements. The government must clearly explain what was corrected and why.

The government follows accounting rules called GRAP Standards. These rules are issued by the ASB. Sometimes the ASB changes an existing rule. Sometimes the government decides there is a clearer way to record something. This may result in a change in accounting policy.

When this happens, the government usually applies the change to past years as well. This means it adjusts old numbers as if the new accounting rule was always used. It does this by:

- Adjusting the opening balance of the previous year; and

- Restating the old numbers.

It is important to do this because we want to compare “apples with apples” when looking at different years. If the numbers changed all of a sudden because of a new rule, it would be confusing.

Sometimes it is not practical to go back and adjust the old numbers. When this happens, the government must explain this clearly in the Notes to the Financial Statements.

Some assets, like land and buildings used to provide services, may increase in value over time. In some cases, the government updates these values to reflect current market conditions. This is known as revaluation.

If the value of an asset increases, the increase is recorded in a Revaluation Reserve within net assets. It is not treated as profit and does not affect the surplus or deficit for the year. Instead, it increases the entity’s overall net worth.

If the value decreases, the decrease first lowers any existing balance of the revaluation reserve for that asset. Any remaining decrease is recorded as an expense.

Over time, as the asset is used or sold, the amounts in the reserve are moved into accumulated surplus. This shows that net assets include more than just cash. They also include changes in the value of infrastructure, land, and buildings held for service delivery.

Reserves are special savings set aside for a specific purpose like housing or infrastructure repair. The statement shows if the government added money to these savings or spent some during the year.

What does this statement show?

You will see a table that tracks each type of net assets. It usually shows:

- Opening balance (what the government started with at the beginning of the year).

- Changes during the year (includes the surplus/deficit, corrections of old mistakes, and transfers).

- Closing balance (what is left at year end).

Example

Government Entity Annual Financial Statements

Statement of Changes in Net Assets as at 31 March 2026

| Figures in Rand thousand | Note(s) | Accumulated Surplus/Deficit |

Reserves | Total Net assets |

|---|---|---|---|---|

| Opening Balance as Previously Reported | 1 | 45 000 000 | 10 000 000 | 55 000 000 |

| Adjustments | ||||

| Changes in Accounting Policies (effect of adjustments in the prior years). | (500 000) | — | (500 000) | |

| Correction of Prior Period Errors | 250 000 | — | 250 000 | |

| Restated Balance at 01 April 2024 | 44 750 000 | 10 000 000 | 54 750 000 | |

| Surplus for the year | 3 200 000 | — | 3 200 000 | |

| Capital Contributions from Government | 1 500 000 | — | 1 500 000 | |

| Revaluations | — | 2 800 000 | 2 800 000 | |

| Balance at 31 March 2025 | 49 450 000 | 12 800 000 | 62 250 000 | |

| Surplus for the year | 4 100 000 | — | 4 100 000 | |

| Gov Capital Withdrawals | (800 000) | — | (800 000) | |

| Revaluations | — | 1 200 000 | 1 200 000 | |

| Balance at 31 March 2026 | 52 750 000 | 14 000 000 | 66 750 000 | |

🔗 Let's connect the dots to other government reports

The Plan: The APP/SDBIP set out specific goals for the year. These could be the number of houses to be built or kilometres of road to be paved. These plans link long-term promises to the money available this year.

The Link: At the end of the year, the surplus or deficit is added to the accumulated surplus in the Statement of Changes in Net Assets. This helps show if the year’s plans were done within available resources. If the government makes deficits year after year, it may have to reduce future plans or find more funding.

The Plan: The Budget is the financial plan for the year. It shows where money will come from. This could be from taxes, grants, or loans. It also shows how it will be spent on services and big projects.

The Link: The Statement of Changes in Net Assets shows how these budget choices affected the government’s finances. For example, if the government decided to move money into a “Replacement Reserve” to buy new ambulances in future, that movement is seen here.

To understand the full picture, you should read this statement together with the Statement of Comparison of Budget and Actual Amounts to see why the plan changed. It should also be read with the Cash Flow Statement to see if they actually had the cash to back up their budget choices.

Citizen Tip: What does this mean for you?

This statement shows whether government’s financial position is improving or getting worse over time.

But numbers alone are not enough.

👉 Always ask:

- Is this growth helping improve services?

- Can government sustain this in the future?

- Does the cash position support what is reported?

To get the full picture, read this statement together with:

- The Statement of Financial Performance (what happened this year)

- The Cash Flow Statement (where the cash went)

- The Budget vs Actual Statement (what was planned vs delivered)

- The Annual Report (what services were actually provided)

Real understanding comes from connecting the numbers to service delivery.